Quick Briefing

- Here's the scoop: that gold and silver 'crash' wasn't actually a fundamental collapse. It was a classic leverage flush – way too many people were stacked in highly leveraged long positions, especially in silver, and when the macro tide turned (Fed got hawkish), it triggered a self-reinforcing cascade of liquidations.

- The big picture is, this isn't gold or silver going bust. Their long-term story as inflation hedges and safe havens is still intact. This whole event was a massive 'reset' that flushed out the excess speculation, potentially creating some sweet entry points for smart money and patient capital who waited on the sidelines.

- But, keep your eyes peeled: short-term volatility is probably sticking around while the market finds its feet. Plus, the real movers are still real yields, the dollar, and the Fed's next moves – those will dictate the medium-term direction more than anything else.

The recent sell-off in gold and silver has been widely labelled as a “crash,” however that description oversimplifies what actually occurred. The move was not driven by a sudden deterioration in the intrinsic value of precious metals. It was the result of extreme positioning, elevated leverage, and a rapid macro repricing that exposed how fragile market structure had become.

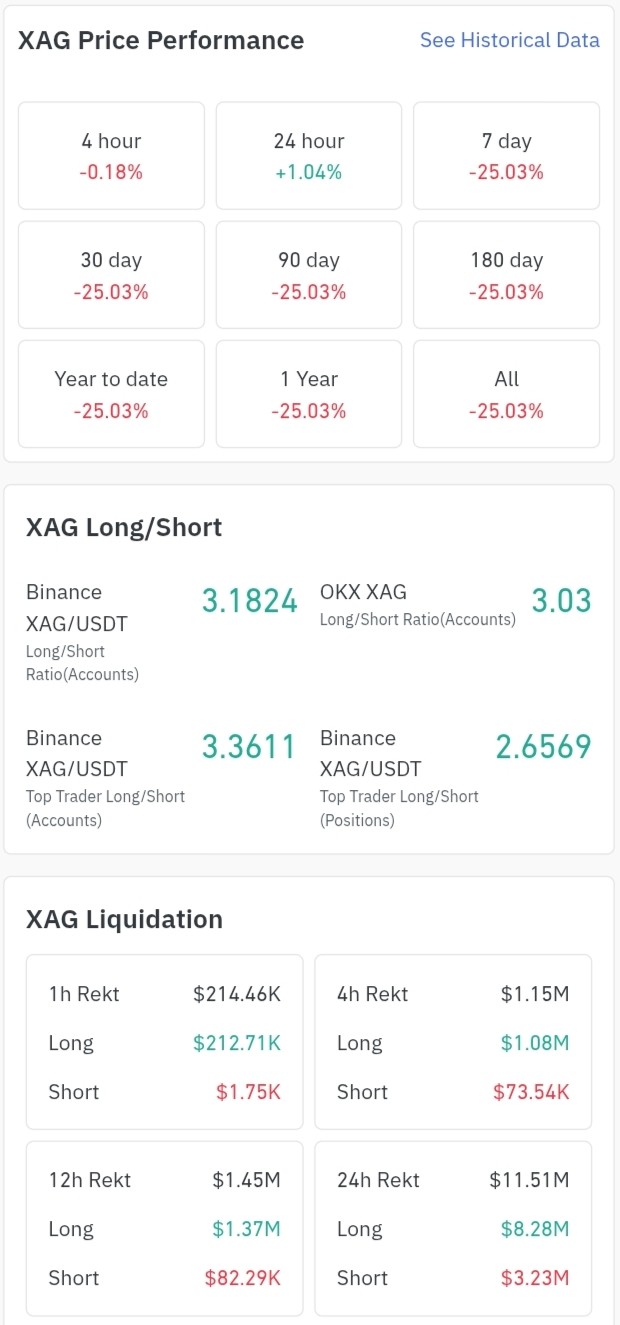

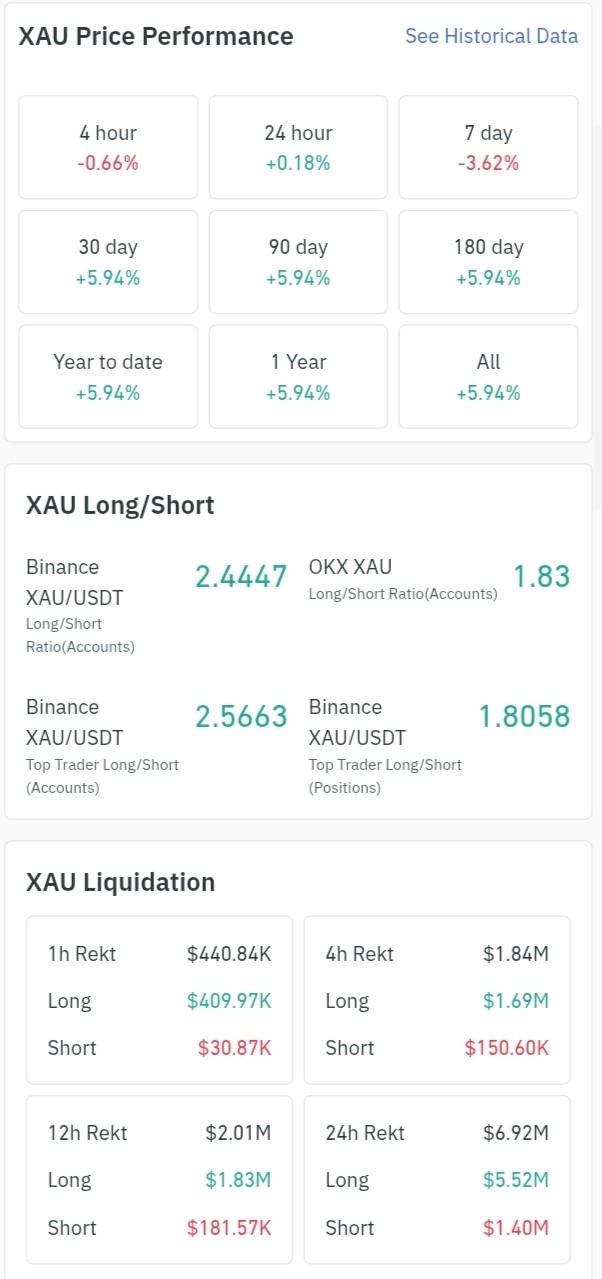

Only days before the decline, gold was trading near $5,500–$5,600 per ounce, while silver had advanced toward $110–$120 per ounce. These levels followed a prolonged and steep rally. Sentiment across both institutional and retail channels had turned heavily one-sided, with precious metals increasingly treated as a guaranteed safe haven and a one-directional trade.

Historically, gold and silver are slow, macro-driven markets. Even meaningful corrections tend to develop over weeks or months, not in a matter of sessions. Silver has experienced very few disorderly collapses in modern history, the most notable being the 1980 Hunt brothers episode. When price dislocates this rapidly, it is usually a signal of structural stress rather than fundamental breakdown.

The initial catalyst was a shift in U.S. monetary expectations. Ongoing hawkish signalling from the Federal Reserve, declining probability of near-term rate cuts, and renewed uncertainty around future policy direction lifted real yields and supported the U.S. dollar. This environment is typically unfavourable for non-yielding assets such as gold and silver.

Under normal conditions, this backdrop should have produced a controlled pullback.

It did not.

The magnitude of the move was driven by positioning and leverage.

- Gold long/short ratios near 2.4–2.5

- Silver long/short ratios above 3.0

These readings indicate a market heavily skewed toward long exposure. When positioning becomes this crowded, downside risk increases sharply because incremental buyers are limited while forced sellers accumulate below price.

At the same time, access to high-leverage silver derivatives expanded following the introduction of $XAG/USDT products on Binance. Trading volume quickly exceeded $4 billion, drawing significant speculative capital into a comparatively thin market.

High leverage fundamentally alters price behaviour.

- Small adverse moves trigger liquidations

- Liquidations generate automatic market sell orders

- Those orders push price lower and activate additional liquidations

The process becomes self-reinforcing.

Silver, due to its thinner depth and higher speculative participation, broke first. As margin calls propagated, traders reduced exposure across correlated assets, including gold. Gold did not collapse because its long-term thesis failed. It declined because portfolios were forced to de-risk.

It is also important to clarify the concept of “value wiped out.”

If gold declines from $5,600 to $4,900, the seller realises a loss. The buyer acquires the same asset at a lower price. The value has shifted between participants. In derivatives markets, losses from liquidated longs flow to short sellers, market makers, and exchanges via fees and funding. Capital does not disappear. It is redistributed.

Large liquidation events historically favour participants with patient capital.

- Institutions tend to accumulate during forced selling

- Retail capitulates near extremes

- Exchanges benefit from elevated volume and fee generation

This episode does not signal the end of gold or silver as monetary assets.

It does not invalidate long-term drivers such as central bank demand, inflation hedging, or geopolitical risk. It represents a reset of excess leverage and speculative positioning.

Excess was flushed.

Positioning is cleaner.

Short-term volatility may persist while open interest stabilises. Medium-term direction will depend primarily on real yields, the dollar, and the evolution of central bank policy.

The core conclusion is straightforward:

- This was not a fundamental collapse.

- It was a structural deleveraging event.

About Meow Alert

Crypto analyst and researcher with 13k+ followers on Binance Square. Focused on on-chain data and market structure.