Quick Briefing

- Here's the scoop: Despite all the market chatter, the Fed isn't cutting rates anytime soon. The latest November and December data shows inflation is stuck above their target, the job market is just cooling down (not collapsing), and the economy is slowing gently. Basically, the conditions for a rate cut just aren't there yet.

- What this means for us: That big, liquidity-driven crypto upside we all crave isn't happening based on macro right now. We need actual catalysts like ETF flows and real network activity to move the needle, not just wishful thinking about Fed easing.

- The big thing to watch out for: Don't get caught buying into the hype. The Fed won't even consider cutting rates until inflation convincingly hits their 2% target, or the job market seriously crumbles (think negative payrolls or unemployment spiking). Until then, expect "higher for longer" interest rates to be the name of the game.

Expectations for a near-term Federal Reserve rate cut have re-emerged across financial markets. However, a review of the latest U.S. macroeconomic releases from November and December suggests that the underlying conditions for policy easing are still not in place.

Inflation remains above target, labor markets are cooling but stable, and growth indicators point to moderation rather than contraction. Taken together, the data continues to support a hold in policy rates rather than an imminent shift toward easing.

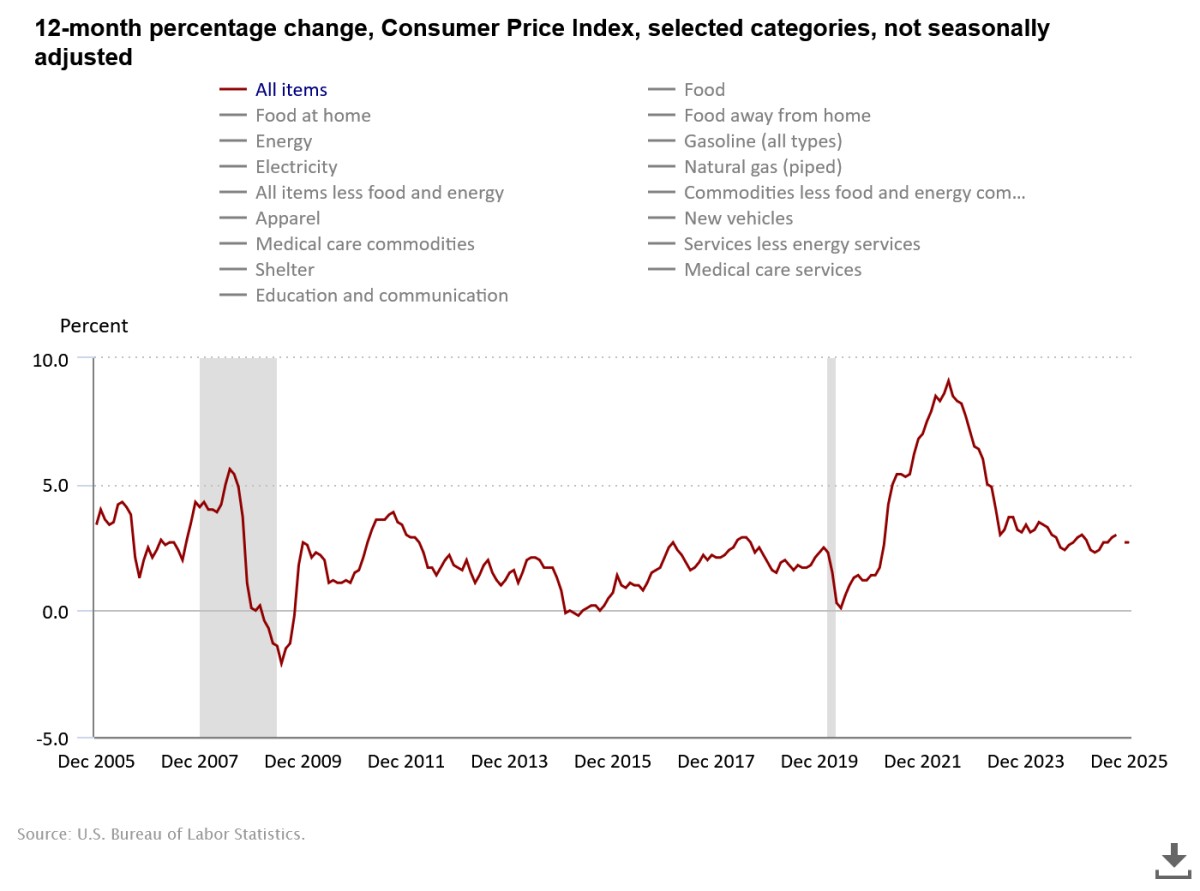

Inflation: Progress Has Plateaued

Headline consumer inflation registered 2.7% year-over-year in both November and December, showing no meaningful decline across two consecutive months. Core CPI has also remained around 2.6%–2.7%, reinforcing the view that disinflation momentum has slowed.

While inflation is significantly lower than its 2022 peak, the Fed’s objective is not simply lower inflation, but inflation that is convincingly converging toward its 2% target. Flat readings near 2.7% do not meet that standard.

Sourec: BLS.gov

For policymakers, cutting rates while inflation is stalled at these levels would risk re-accelerating price pressures, especially in services and housing-related components.

In practical terms, inflation is lower, but not yet low enough.

Labor Market: Cooling Without Deterioration

Employment data indicates a gradual loss of momentum rather than structural weakness.

- November nonfarm payrolls: +64,000

- December nonfarm payrolls: +50,000

- Unemployment rate: 4.6% in November, easing to 4.4% in December

Source: https://www.investing.com/economic-calendar/nonfarm-payrolls-227

Job creation has slowed materially compared with prior years, but remains positive. Historically, the Federal Reserve has begun easing only after payroll growth turns negative or unemployment rises persistently.

Weekly initial jobless claims remain near 200,000, a level consistent with a relatively healthy labor market and limited layoff activity.

This combination suggests softening, not stress.

Growth Backdrop: Soft Landing Still Intact

The broader economic picture points to decelerating activity rather than recession. Consumption growth has cooled, business investment is selective, and financial conditions remain restrictive, yet there are few signs of systemic strain.

For the Federal Reserve, this environment argues for patience. The central bank’s priority remains ensuring inflation returns to target without prematurely loosening policy.

A soft landing, while challenging, is still the base case.

Policy Messaging and Political Noise

Recent commentary from Federal Reserve officials continues to emphasize data dependence and caution. Policymakers have avoided signaling urgency toward easing, instead stressing the need for greater confidence that inflation is sustainably moving lower.

Political pressure for rate cuts has increased, but it has not altered the Fed’s communication.

Separately, Treasury Secretary Scott Bessent has recently spoken about building a more constructive regulatory framework for digital assets. Markets have interpreted this as a potentially positive long-term signal for the crypto sector. However, regulatory posture and monetary policy operate on separate tracks.

Improved regulatory tone does not equal imminent monetary easing.

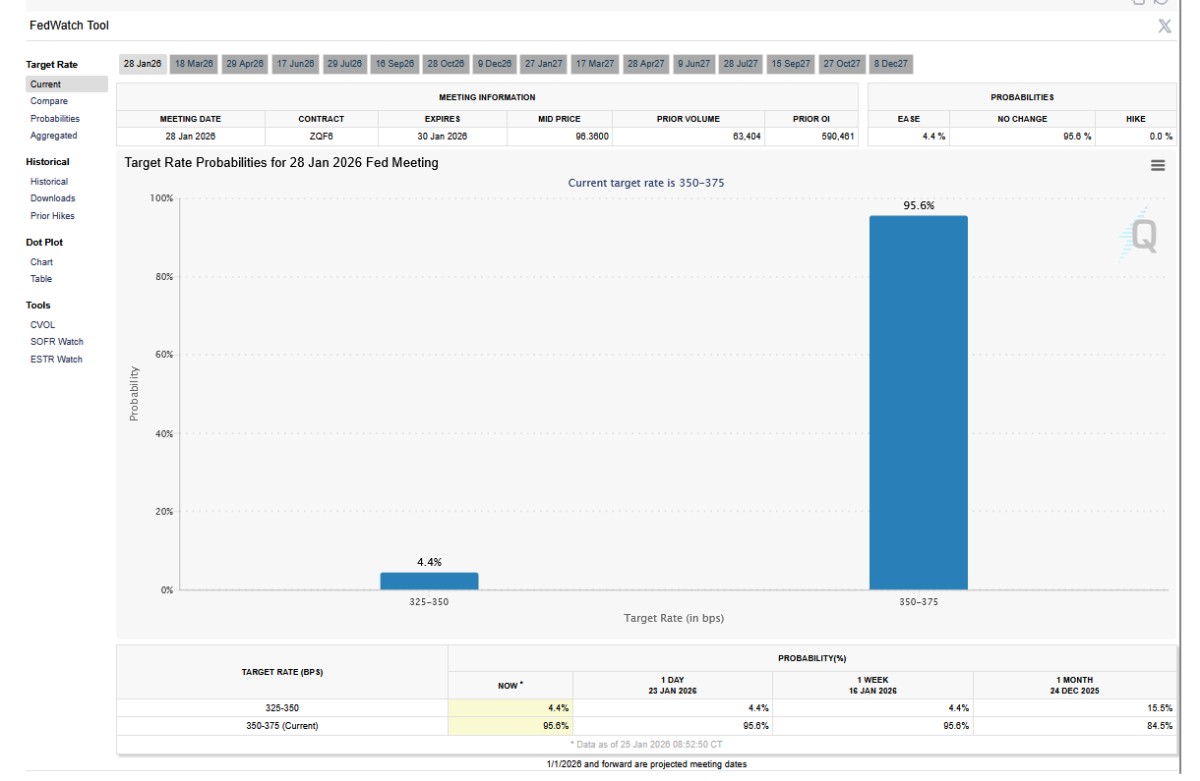

Market Pricing Reflects Reality

Interest rate futures currently assign approximately:

- 96% probability of no rate change at the next FOMC meeting

- 4% probability of a rate cut

Source: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Just a month earlier, cut probabilities were meaningfully higher. The repricing reflects the November–December data showing inflation stabilization and labor resilience.

Markets have adjusted to the same conclusion policymakers are drawing.

What Would Justify a Cut

A material shift toward easing would likely require a combination of:

- CPI and Core PCE moving decisively toward 2.0%–2.2%

- Payroll growth turning negative

- Unemployment rising toward 5% or higher

- Jobless claims climbing consistently above 260k–300k

Absent these developments, the threshold for rate cuts remains unmet.

Implications for Crypto Markets

For digital asset markets, the macro environment remains neutral to mildly restrictive.

Without a near-term Fed pivot:

- Liquidity-driven upside is limited

- Price action is more dependent on ETF flows, network activity, and sector-specific catalysts

- The next macro-driven bull phase likely begins only once markets start pricing genuine easing, not speculation about easing

In short, macro is not yet a tailwind.

Conclusion

November and December data present a consistent picture.

Inflation is stuck above target.

Labor markets are cooling but stable.

Growth is slowing, not contracting.

This is not the backdrop for a Federal Reserve pivot.

Rate cuts remain a future possibility, not a near-term policy path. Until inflation resumes a clear downward trend or labor markets weaken materially, the Fed is positioned to maintain a restrictive stance.

For investors, the implication is straightforward: expect higher-for-longer policy to persist, and position accordingly.

About Meow Alert

Crypto analyst and researcher with 13k+ followers on Binance Square. Focused on on-chain data and market structure.

Intelligence Stream

BTC Near $80K — Data Shows Liquidity Build, But Macro Is Holding It Back

17 Reads

Author Update

Europe’s Rate Hike Signal: A Liquidity Shift That Crypto Markets Are Underestimating

20 Reads

Author Update

Trump Loses Tariff Power: Why This Could Trigger the Next Crypto Bull Run

27 Reads

Author Update