Quick Briefing

- Here's the scoop: Kevin Warsh, a seasoned player from Wall Street, the White House, and the Fed during the '08 crisis, is a strong contender for future Fed Chair. His core philosophy? The Fed should be a crisis stabilizer, not a perpetual asset inflator. He's all about discipline, credibility, and using emergency tools only when truly needed, not to smooth every bump.

- Why this matters: For crypto, this could be a big deal. Warsh sees Bitcoin as a signal and wants regulation that brings legitimacy, favoring transparent assets and strong infrastructure over opaque leverage. This means better long-term health for the real crypto economy, but less tolerance for the wild, liquidity-fueled parabolic runs. For broader markets, think fewer blanket stimulus programs, more focus on company fundamentals for equities, and a potentially stronger dollar due to a more credible central bank.

- What to watch out for: If Warsh steps in, don't expect another round of massive, easy-money stimulus or endless QE like we saw post-2020. This could be a tougher environment for highly leveraged trades and speculative "meme coin" type rallies. While it aims for long-term health, the short-term squeeze on opaque crypto practices, offshore loopholes, and unsupervised credit could be intense. Basically, the "liquidity miracle" days might be behind us, so focus on real value and robust projects.

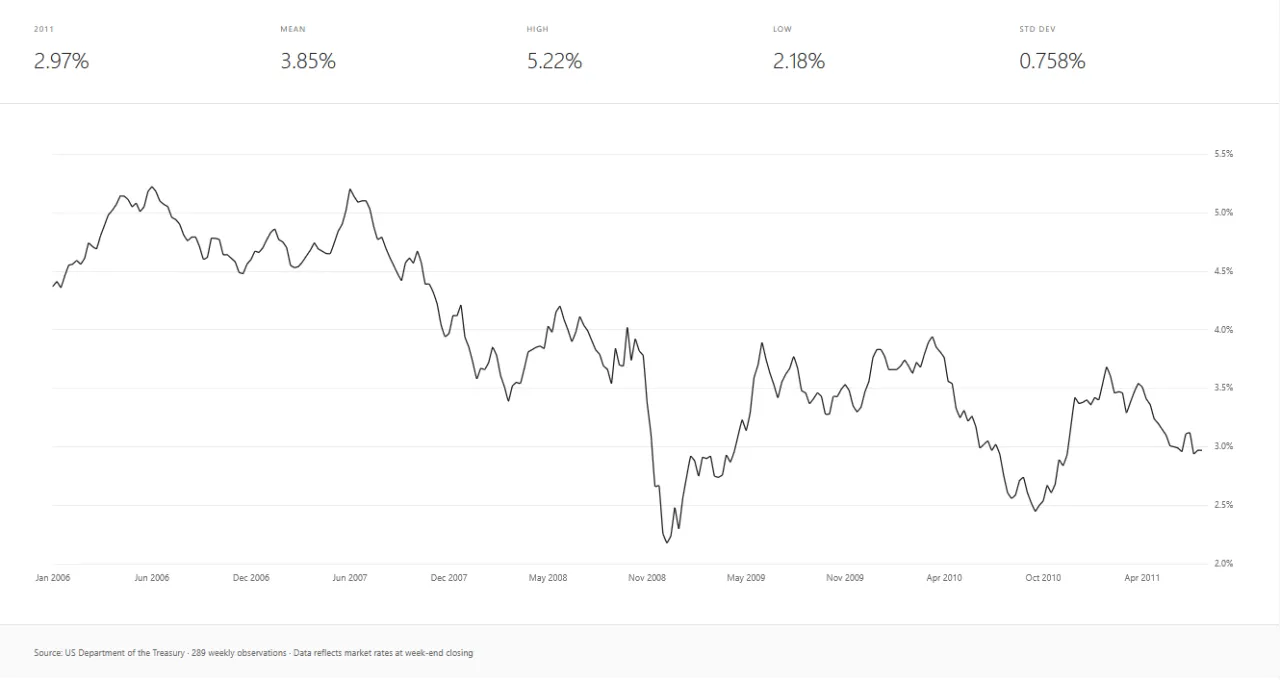

Kevin Warsh built his career across three systems that rarely overlap cleanly: Wall Street, the White House, and the Federal Reserve. He began at Morgan Stanley in mergers and capital markets, where deal flow, leverage, and liquidity are not academic concepts but daily realities. He later moved into government as a senior economic adviser in the George W. Bush administration before being appointed to the Fed’s Board of Governors in 2006. His entire Fed tenure ran through 2011, meaning he was in the room during the 2008 global financial crisis, the collapse of Lehman Brothers, the creation of emergency lending facilities, and the first large-scale quantitative easing programs.

At that time, the Fed’s balance sheet expanded from under $900 billion in 2007 to over $2 trillion by 2009. Warsh supported emergency action, but he also began warning early about the risks of letting extraordinary tools become permanent policy. That tension between necessity and restraint still defines his thinking.

Core Policy Philosophy

Warsh’s philosophy is not ideological. It is operational.

He believes central banks must step in when the financial system is at risk of collapse. He does not believe central banks should exist to continuously inflate asset prices or smooth every downturn.

Three ideas appear repeatedly in his speeches and writing:

- Monetary policy should stabilize the system, not engineer perpetual asset growth

- Large balance sheets carry long-term costs even when short-term benefits look attractive

- Credibility is a central bank’s most valuable asset

In plain terms: crisis tools are for crises, not for normal economic cycles.

Rates vs Balance Sheet: A Crucial Distinction

Most market participants mentally link rate cuts with liquidity expansion. Warsh does not. He treats interest rates and the balance sheet as separate levers.

What this means in practice:

- Rates can fall if inflation is clearly trending toward target (around 2%)

- Balance sheet growth is not automatic just because rates fall

- Forward guidance should be limited so the Fed is not locked into long promises

For context, during the 2020–2022 period the Fed cut rates to 0–0.25% and expanded its balance sheet to roughly $9 trillion. A Warsh-style framework would likely avoid repeating that pairing. Lower rates could happen. Massive QE at the same time would be far less likely.

Political Context and Succession

Warsh has been publicly supported by Donald Trump as a preferred future Fed chair. Jerome Powell’s term ends in 2026, which is why positioning around Warsh has started early.

Markets see a mixed message:

- Potentially easier rates than today

- Tighter long-term discipline than the post-2020 era

That mix explains why bond yields and the dollar often react positively to Warsh-related headlines, while risk assets react more cautiously.

Warsh’s Take on Crypto

Warsh is neither pro-crypto nor anti-crypto in an ideological sense. He has described Bitcoin as an important asset and, more importantly, as a signal. A signal that some investors seek alternatives when confidence in traditional monetary management weakens.

His broader instincts suggest:

- Crypto markets should exist

- Crypto markets should be regulated

- Systemic risk inside crypto should not be ignored

How Analysts Interpret a Warsh-Led Fed

- Fewer blanket stimulus programs

- Faster removal of emergency support once stress passes

- Less tolerance for asset bubbles justified by policy

Market Impact Outlook

Possible Paths Forward

Political Delay Case

Confirmation battles slow change. Powell-era framework persists longer.

Bottom Line

About Meow Alert

Crypto analyst and researcher with 13k+ followers on Binance Square. Focused on on-chain data and market structure.