Quick Briefing

- Here's the scoop: While most folks were panicking and taking losses as Bitcoin's price dropped between November and February, big institutions like MicroStrategy and Tether were actually scooping up tons of BTC. They weren't selling; they were buying cheap from all the "forced sellers" – think leveraged traders getting liquidated and short-term players bailing out. It was a massive transfer of ownership from weak hands to strong, patient ones.

- The big picture is this is a totally new game compared to past cycles. Instead of big players dumping on retail during highs, they're now accumulating during fear. This means a huge chunk of Bitcoin supply is moving into hands that aren't worried about short-term swings or margin calls. It reshapes who really controls the supply, potentially setting the stage for more stability and upside when the market eventually turns, as these new owners are "built to wait."

- But here's the catch: this shift doesn't mean prices are going to skyrocket tomorrow. Institutions are accepting some hefty paper losses right now due to accounting rules, even while buying more. So, while they're built for the long haul, watch out for continued market instability; their conviction will be tested if the slump drags on, and it won't magically prevent more short-term pain for the impatient.

The market is weak right now. Price stays under pressure, rebounds fail quickly, and confidence is thin. In this kind of environment, most participants focus on what is going wrong. Institutions focus on something else: who is being forced to sell. That difference explains why losses are piling up on one side of the market while accumulation continues on the other.

Between November and February, Bitcoin did not break. Ownership shifted.

Weak markets reveal forced sellers

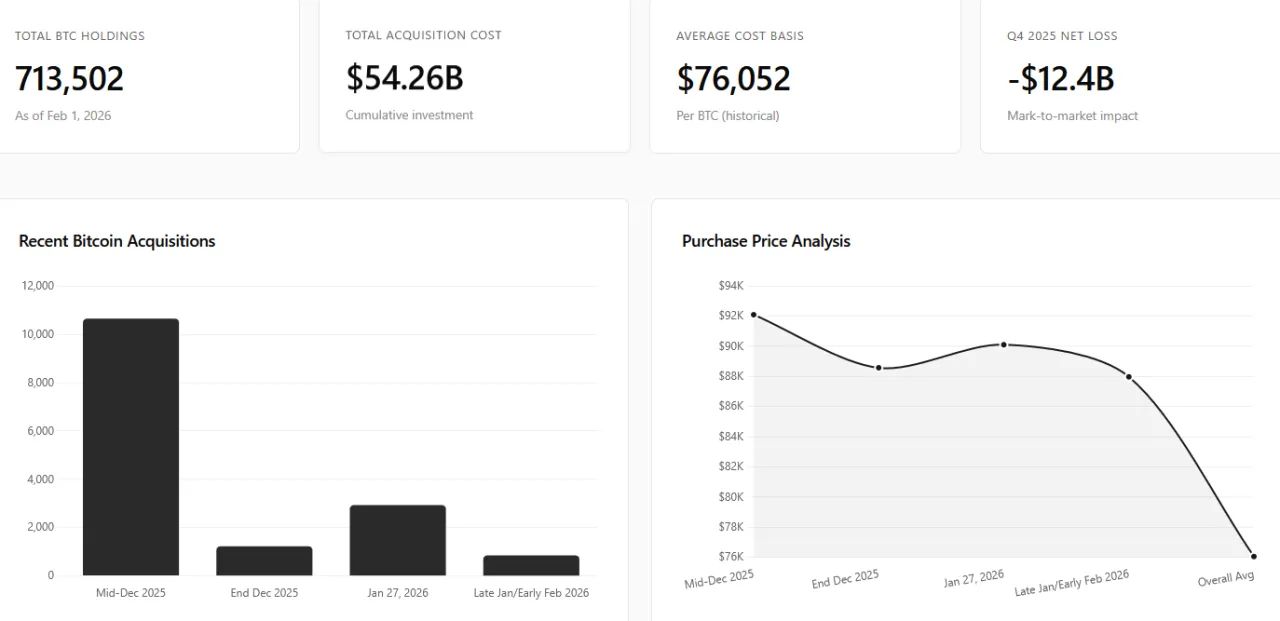

MicroStrategy: buying while reporting losses

Accumulation:

- November 2025: about 8,700 $BTC added

- December 2025: about 11,800 BTC added

- January 2026: about 41,000 BTC added

- Total holdings by early February: roughly 713,500 BTC

- Estimated average cost: around $76,000 per BTC

- Q4 2025 reported loss: around $12.4B, largely from accounting impairment

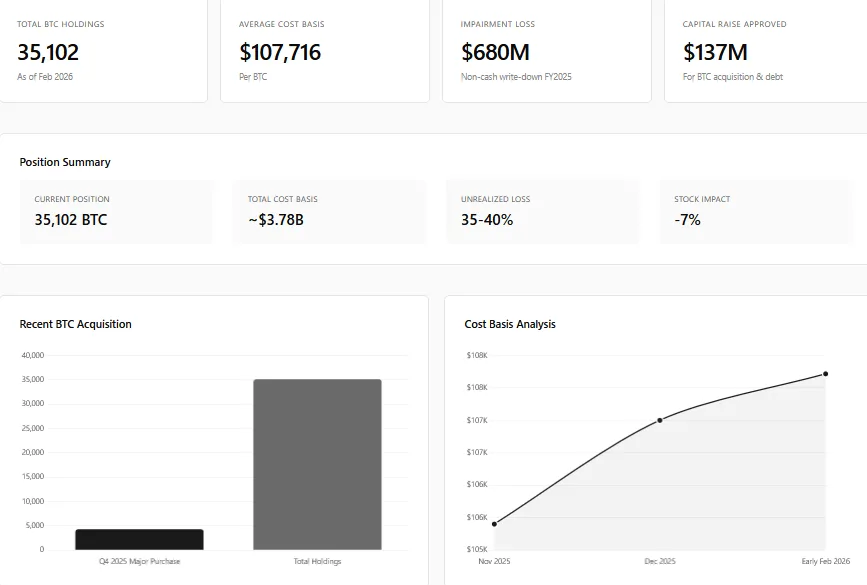

Metaplanet: the same logic, smaller scale

- Q4 2025 purchases: about 4,279 BTC

- Total holdings by early 2026: about 35,102 $BTC

- Estimated average cost: around $107,700 per BTC

Reported impact:

- Accounting impairment: about $680M

- Funding raised through equity, warrants, and debt, including plans for up to $137M in new capital

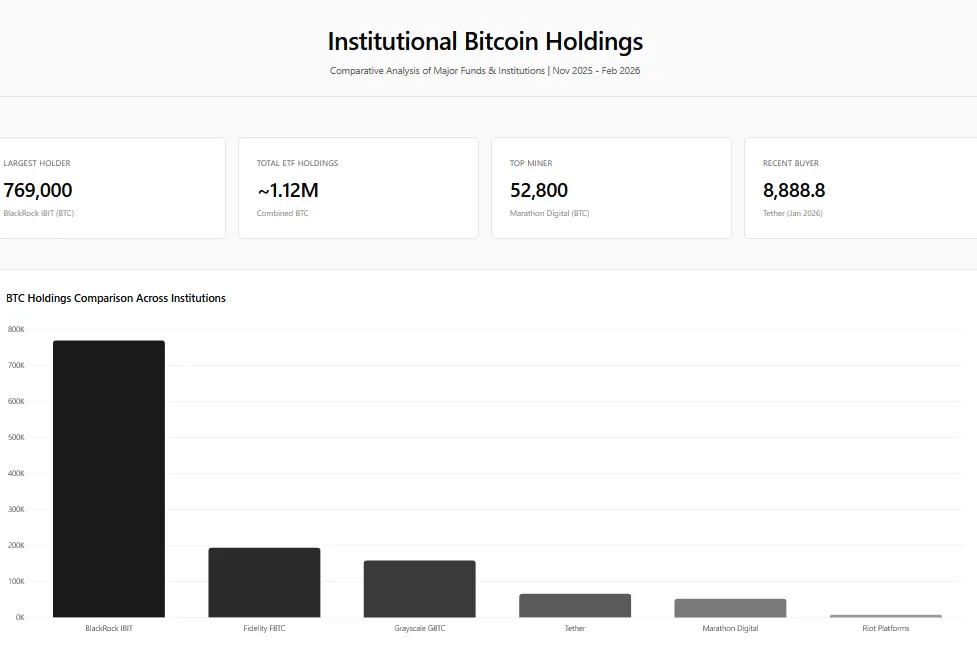

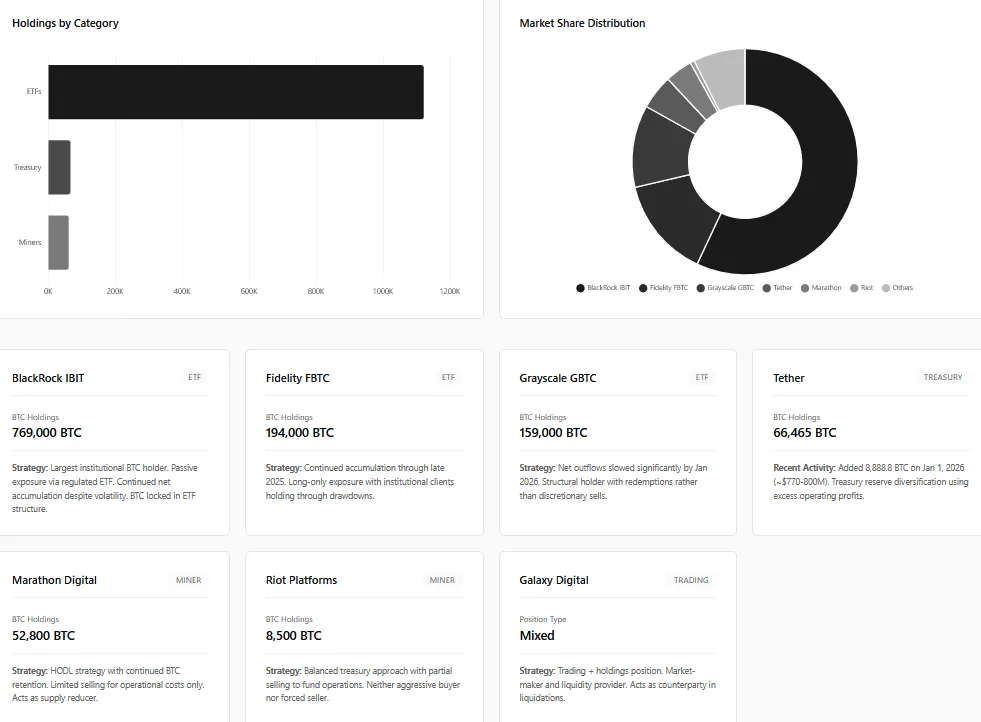

Other large holders showed similar behavior

- Tether added 8,888.8 BTC in January 2026 using operating profits. This Bitcoin is treated as a reserve asset, not a short-term position.

- Spot ETFs such as BlackRock iShares Bitcoin Trust and Fidelity Wise Origin Bitcoin Fund continued holding large amounts of BTC. Investor redemptions occurred, but the underlying Bitcoin largely stayed inside regulated custody.

- Mining companies like Marathon Digital limited selling despite margin pressure, choosing to retain BTC rather than distribute it aggressively into weakness.

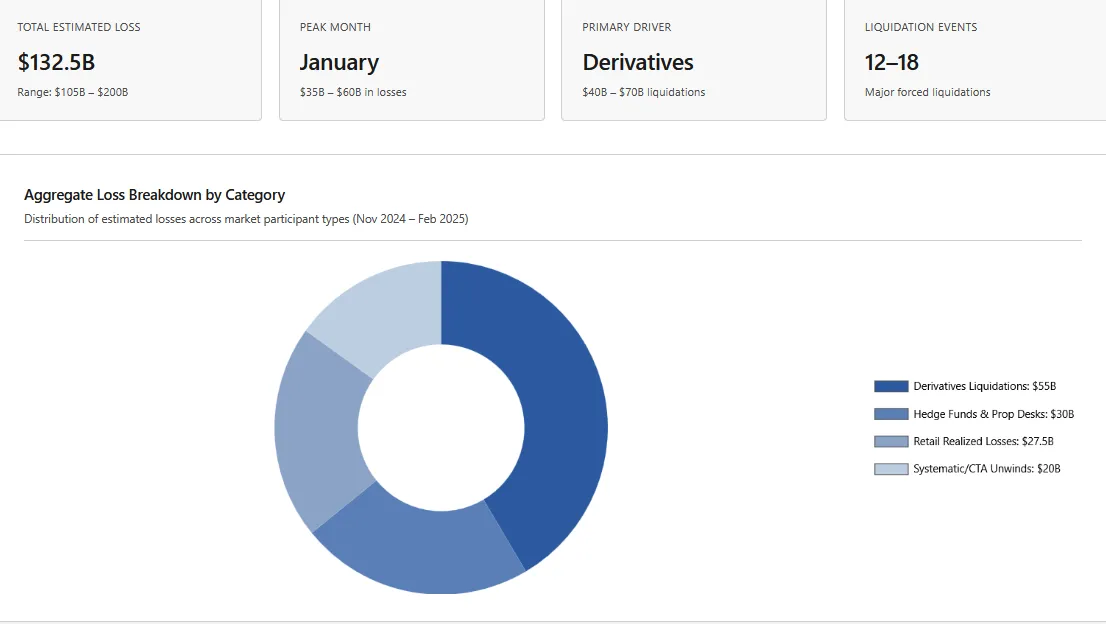

Where the real losses occurred

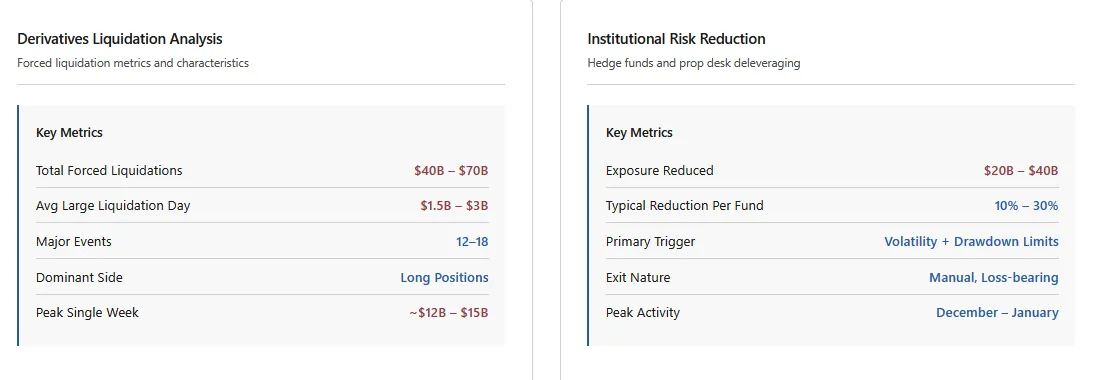

Derivatives markets absorbed the first impact. Repeated liquidation waves across Bitcoin and correlated assets removed an estimated $40–70 billion in notional long exposure. Many of these liquidations occurred during failed rebounds, where leverage was rebuilt and then flushed again. These exits were forced and executed without regard for price.

How this cycle differs from older ones

The role of structure and psychology

- No margin calls

- Long-duration funding

- Acceptance of accounting drawdowns

- No urgency to be right immediately

Take

- Institutions accumulated tens of thousands of $BTC

- Reported losses increased while holdings grew

- Real losses fell on leveraged and short-term participants

- Supply moved into hands with no urgency to sell

About Meow Alert

Crypto analyst and researcher with 13k+ followers on Binance Square. Focused on on-chain data and market structure.